Modern merchants often find themselves walking a precarious tightrope where every security measure intended to stop a criminal simultaneously threatens to alienate a loyal customer. In the current digital economy, the traditional defensive stance of risk management is undergoing a significant transformation. Rather than simply blocking threats, businesses are shifting toward a proactive growth strategy that treats payment security as a revenue driver. This evolution recognizes that rigid, outdated protocols do more than just deter hackers; they create unnecessary hurdles for legitimate buyers who demand seamless experiences.

Over-correcting for risk frequently results in a catastrophic loss of customer trust. When a checkout process becomes overly cumbersome, a shopper is likely to abandon their cart and migrate to a competitor with a smoother interface. The challenge lies in distinguishing between a high-risk intruder and a high-value patron who might simply be shopping from a new location or device. By moving away from a fortress-mentality, organizations are finding that profitability depends on a nuanced understanding of risk that prioritizes the preservation of the customer relationship over the sheer prevention of every single suspicious attempt.

Why Every Blocked Transaction Might Be Costing You More Than Fraud Itself

The shift in risk management reflects a broader understanding that friction is often the silent killer of conversion rates. While a transaction blocked by a fraud filter prevents a single instance of theft, it can also permanently sever the connection between a brand and a lifetime user. In a marketplace where customer acquisition costs are rising, losing a vetted buyer to a false positive is a luxury no business can afford. Consequently, the industry has begun to view every declined transaction not just as a security check, but as a potential missed opportunity for long-term loyalty.

Proactive growth strategies now require a balance where security acts as an invisible layer rather than a visible barrier. By implementing smarter detection methods, companies are reducing the cognitive load on the consumer. This approach ensures that while the backend infrastructure remains vigilant against evolving threats, the frontend experience remains fluid. Merchants who successfully manage this balance are discovering that their most valuable customers are those who feel both secure and unburdened by the platform, leading to higher repeat purchase rates and improved financial health.

The Economic Reality of Revenue Leakage in Modern E-Commerce

Financial health in the e-commerce sector is increasingly threatened by a persistent 3.2% global revenue loss attributed directly to fraudulent activities. While the theft of funds is the most visible issue, the economic reality of revenue leakage extends far deeper into the operational budget. Companies are often blindsided by ancillary expenses such as chargeback fees, the cost of lost physical goods, and the administrative burden of manual transaction reviews. These compounding costs can erode profit margins, especially in industries where competition is fierce and the room for error is slim.

The primary driver of these losses is the fragmentation of data within internal systems. Many organizations operate with siloed information, where identity verification tools do not communicate with payment history logs or behavioral tracking software. This lack of integration creates significant blind spots that sophisticated bad actors exploit with ease. By moving through different gaps in the security perimeter, fraudsters can mimic legitimate behavior, making them nearly impossible to detect with traditional, isolated tools. Solving this problem requires a departure from disjointed security stacks toward a unified intelligence model.

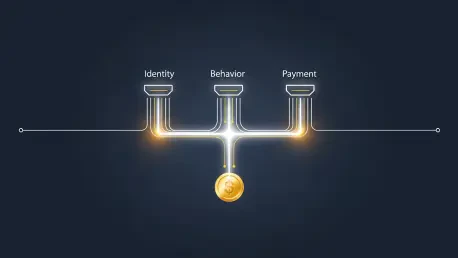

Breaking Down the Integrated Payments Protection Framework

Transitioning to an integrated payments protection framework involves moving beyond the checkout button to secure the entire customer journey. This end-to-end model starts at the moment of account creation and persists through login, transaction, and even post-purchase interactions. By monitoring the complete lifecycle of a user, businesses gain the context necessary to make informed decisions. This approach prevents problems before they occur at the payment stage, effectively thinning the herd of potential threats long before a credit card is even involved.

At the heart of this framework is the consolidation of identity verification, payment history, and real-time behavioral data into a single, unified profile. When these data points converge, the resulting risk assessment becomes significantly more accurate. For instance, a transaction that might look suspicious in isolation can be validated if the system recognizes the device fingerprint and historical spending patterns of the user across other platforms. Consolidating this information reduces the reliance on broad, imprecise rules, allowing for higher approval rates and a more personalized security experience for every shopper.

Leveraging Expert Insights to Balance Risk and Revenue

Insights from the Merchant Risk Council and Equifax shed light on the staggering hidden costs of modern security measures, revealing that false declines can lead to 75 times more lost revenue than actual fraud. This statistic serves as a wake-up call for executives who have historically prioritized risk mitigation above all else. A false decline does more than lose a single sale; it often permanently damages the reputation of a brand in the eyes of a frustrated consumer. The focus must shift toward balancing the scales to ensure that the pursuit of security does not result in the destruction of legitimate commerce.

To achieve this balance, leading firms are implementing a sophisticated feedback architecture. This system allows the risk model to learn from every outcome, whether it was a successfully blocked fraud attempt or a legitimate transaction that was accidentally flagged. By continuously feeding these results back into the primary engine, the software refines its predictive capabilities. This iterative process ensures that the security experience becomes progressively smoother for loyal users, effectively turning historical data into a strategic asset that supports higher conversion rates and long-term customer loyalty.

Strategic Steps for Implementing a Profit-Centric Risk Model

Implementing a profit-centric risk model required the strategic automation of decision-making through artificial intelligence. By utilizing advanced algorithms to handle clear-cut “yes” or “no” scenarios, businesses eliminated the bottlenecks associated with human intervention. This automation allowed specialized risk teams to step away from routine approvals and focus their expertise on complex, high-value exceptions that required a more investigative touch. The result was an operation that scaled efficiently without compromising on the quality of scrutiny applied to truly dangerous actors.

Organizing a sustainable risk strategy meant aligning all protocols with regulatory requirements like Anti-Money Laundering and Know Your Customer mandates. By syncing these security layers within a single growth loop, merchants effectively created a barrier against legal liability while maintaining a frictionless user experience. This strategic transition ultimately empowered businesses to convert their risk departments into profit centers. The adoption of these integrated systems ensured that profitability stayed ahead of the curve as the digital payment landscape continued to evolve.